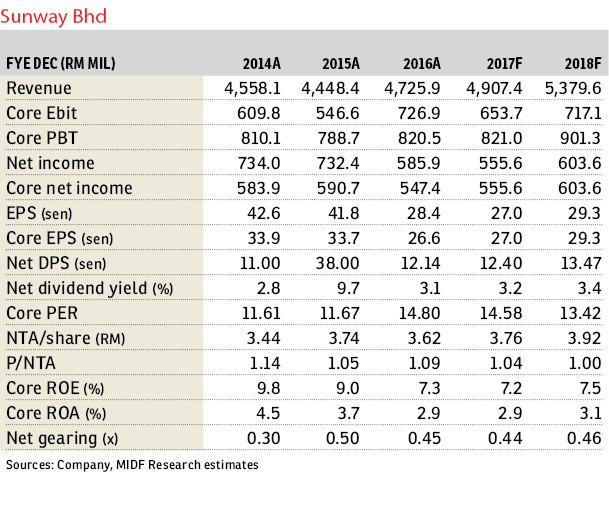

Sunway Bhd (July 14, RM3.96)

Maintain neutral with a revised target price (TP) of RM3.82: Sunway Bhd announced that it has entered into a sale and purchase agreement to acquire 4.53 acres (1.83ha) of freehold land along Jalan Belfield, Kuala Lumpur, for RM165 million. The expected completion date is in the second half of 2017 (2H17).

We view the land acquisition positively as it improves the company’s sales outlook for financial year 2018 (FY18). The land will be acquired with approvals obtained for a mixed-use development with a plot ratio of 8.81 times, indicating projects on the land will be readily launched.

Proposed development on the land will be primarily serviced apartments with some lifestyle retail units. The estimated gross development value (GDV) of the proposed development is at approximately RM1.1 billion, translating into a land cost to GDV ratio of 15% which is within the industry average.

Meanwhile, the acquisition price of RM836 per sq ft (psf) is higher than the price of RM485psf that Tradewinds Corp Bhd paid for the Jalan Belfield land in 2015 which could be due to the strategic location of the land. The land is located less than 500m from the Maharajalela monorail station, hence we expect the good connectivity to underpin good take-up rates of the project.

Sunway intends to fund the acquisition via internally generated funds and borrowings. We estimate the net gearing of Sunway to be lifted marginally to 0.49 times post acquisition from a net gearing of 0.47 times as of the first quarter of FY17 (1QFY17).

Meanwhile, immediate earnings impact from the land acquisition is limited as the target launch of the proposed development will be in 2H18.

We left our earnings forecast for FY17 to FY18 unchanged as we expect earnings contribution from the proposed development to kick in from FY19 onwards.

Meanwhile, we revised our TP for Sunway upwards to RM3.82 from RM3.64 after taking into account the net present value from the proposed development, and also lowering our discount for its property division to 10% from 20% in view of the improved property market outlook for Johor and the Klang Valley. Our TP is based on sum-of-parts valuation. — MIDF Research, July 14

This article first appeared in The Edge Financial Daily, on July 17, 2017.

For more stories, download TheEdgeProperty.com pullout here for free.

TOP PICKS BY EDGEPROP

Kawasan Perindustrian MIEL

Batang Kali, Selangor

Livia @ Bandar Rimbayu

Telok Panglima Garang, Selangor

Robin @ Bandar Rimbayu

Telok Panglima Garang, Selangor

Penduline @ Bandar Rimbayu

Telok Panglima Garang, Selangor

Penduline @ Bandar Rimbayu

Telok Panglima Garang, Selangor

Chimes @ Bandar Rimbayu

Telok Panglima Garang, Selangor

Taman Tun Dr Ismail (TTDI)

Taman Tun Dr Ismail, Kuala Lumpur

{kind=link}