Property sector

Maintain neutral: Granted, the share price of most of the property developers have moved up this year, which we believe is due to renewed buying interest in laggards and overall improved market risk appetite rather than on signs of recovery in operating conditions.

We are still of the view that the property market will remain challenging this year due to the current difficult trading environment, driven by weak sentiments, low affordability, stricter bank lending and rising incoming supply.

The sector is also faced with high property prices (and high household debt) and oversupply in certain segments — such as high-end condominiums, especially in Iskandar Malaysia. All told, we maintain our “neutral” call on the sector.

We believe property prices will still hold up well, however, supported by ample liquidity, high input costs (due to compliance/land costs), the low interest rate environment and strong secular positives (young demographics and improved connectivity from rail spending).

Flat demand growth is expected. Property sales have continued to soften, with the impact of cooling measures and oversupply concerns in certain markets (mainly in Iskandar Malaysia, Johor). Property developers have mostly set flat sales targets for this year, which signals that property sales are expected to stay moderate at best.

Also, we see heightened competition, especially in the affordable housing segment, with the household income eligibility raised to RM15,000 per month and the reduced moratorium of five years by the government. This, we believe, could further squeeze margins in the crowded affordable housing market.

High property prices seem to be a new norm, especially in developed countries which are still recording new highs despite cooling measures introduced which have successfully reduced transactions.

In normal circumstances, property prices should ease, but in certain markets, property prices are still stubbornly hovering at elevated levels. Cooling measures in Malaysia appear to have successfully slowed down the property price increase somewhat.

The house price index, as a whole, contracted marginally by 0.7% in December 2016. That said, property prices in Malaysia are still considered unaffordable based on recent studies with the median house prices already more than 5.5 times the annual household income (Kuala Lumpur: seven times for residential properties) as compared to three times, which is considered the affordable range.

Consumer sentiment is still weak, with most becoming more concerned about the economy, increasing food prices and political stability, according to the latest Nielsen survey. Household debt levels are still high (albeit easing marginally from 89% of gross domestic product in 2015 to 86.7% in the first quarter of 2017).

All in, we believe growth from credit expansion is unlikely in the near term.

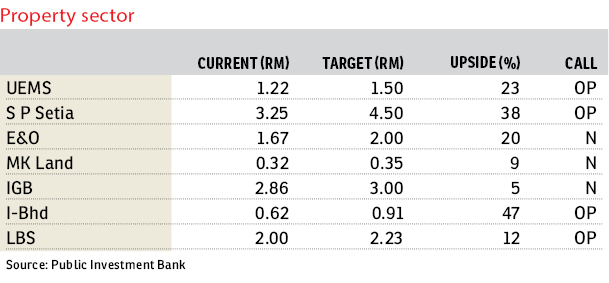

Our sector picks are selected property stocks, such as S P Setia Bhd, UEM Sunrise Bhd and LBS Bina Group Bhd, which have healthy unbilled sales, exposure to growth areas and well-located land banks (especially for S P Setia, which is expected to grow even bigger with the proposed merger with I&P Group Sdn Bhd).

As for UEM Sunrise, the trading environment in Johor is still tough, but we believe the group will be able to regain its sales momentum, given its well-located land banks in the Klang Valley and Iskandar Malaysia. LBS is preferred for its strong exposure to the mid-market segment.

Cooling measures worked as intended. Property transactions resumed their downward trajectory in 2015, with sentiments continuing to be bogged down by the implementation of the goods and services tax which came into effect in April 2015.

We reckon that weak demand could persist, given the high projected incoming supply and cautious sentiments in view of high property prices (despite the drop in transactions) and stricter lending by banks.

That said, the house price index has been holding relatively well. The house price index, as a whole, eased marginally by 0.7% in December 2016. High-rise properties on average dropped about 2% quarter-on-quarter (q-o-q) in December 2016, while the landed house price index was lower by about 3% q-o-q. — PublicInvest Research, July 14

This article first appeared in The Edge Financial Daily, on July 17, 2017.

For more stories, download TheEdgeProperty.com pullout here for free.

TOP PICKS BY EDGEPROP

Springfield Residences @ Setia EcoHill 2

Semenyih, Selangor

Pangsapuri Akasia, Bandar Botanic

Bandar Botanic/Bandar Bukit Tinggi, Selangor

Bandar Bukit Tinggi

Bandar Botanic/Bandar Bukit Tinggi, Selangor

Pangsapuri Akasia, Bandar Botanic

Bandar Botanic/Bandar Bukit Tinggi, Selangor

{kind=link}