- The research house is positive on the deal, as it allows Scientex to expand its footprint and build upon its success in affordable housing in the northern part of Selangor.

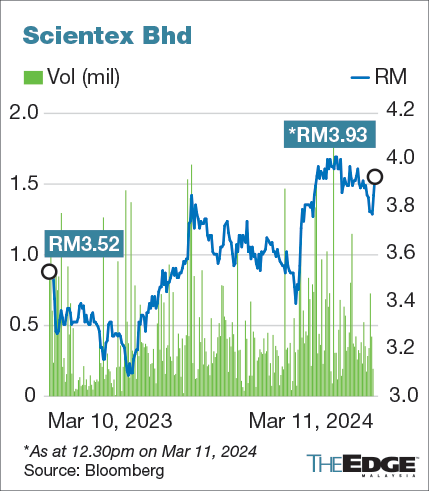

KUALA LUMPUR (March 11): Scientex Bhd shares rose in Monday morning trade, after analysts turned upbeat on its RM335.68 million land acquisition in Batang Berjuntai, Kuala Selangor.

Analysts deem the deal reasonable, and believe it allows for the expansion of the company's footprint in the northern part of Selangor.

At 10.45am, the plastic product manufacturer’s shares were traded at RM3.89 after rising four sen or 1%. At RM3.89, the stock was valued at RM6.03 billion.

Last Friday, Scientex disclosed that its unit Scientex Park (M) Sdn Bhd had entered into a conditional sale and purchase agreement with Metalplex Plantation Sdn Bhd for the proposed acquisition of a parcel of freehold land measuring 826 acres (334.27 hectares).

(Read: Scientex leverages EdgeProp EPIQ for data-driven land acquisition in Malaysia)

TA Securities believes that the proposed acquisition price of RM335.7 million or RM9.33 per square feet (psf) is reasonable, given that the price falls below the recent transacted freehold land price in Bestari Jaya of between RM33 and RM35 psf.

“According to the announcement, the actual GDV (gross development value) of the project is yet to be ascertained. However, we reckon the potential GDV to be around RM4 billion, based on its historical projects in the central region. The acquisition price represents approximately 8.21% of our projected GDV, which is below the threshold of 20%," said the research house in a research note on Monday.

Kenanga Research also noted that the price tag of RM9.33 psf is at a discount price to the asking price for agricultural land in the surrounding areas of between RM12 and RM13 psf.

Kenanga Research attributed this to the location being at a distance away from the Kuala Selangor town area, potentially a low land efficiency owing to land use restrictions and the requirement for additional investment in basic amenities.

The research house is positive on the deal, as it allows Scientex to expand its footprint and build upon its success in affordable housing in the northern part of Selangor.

Post acquisition, Kenanga Research said Scientex’s net debt and net gearing are still highly manageable. Its net debt will increase from RM515 million as at end-October 2023 to RM851 milllion, while its net gearing will rise from 0.15 times to 0.24 times.

Scientex said the proposed acquisition will be funded by internally generated funds and bank borrowings.

For now, TA Securities and Kenanga Research have maintained their earnings forecasts for Scientex, pending the exact GDV and total development cost to be disclosed.

TA Securities expects Scientex to deliver annual net profit of RM534.7 million for the financial year ending July 31, 2024 (FY2024), up from RM438.14 million for FY2023.

It also expects Scientex to deliver annual earnings of RM589.9 million in FY2025, and RM591.7 million in FY2026.

For Kenanga Research, it projected the group to deliver a net profit of RM546.2 million for FY2024, and further growth to RM565.7 million for FY2025.

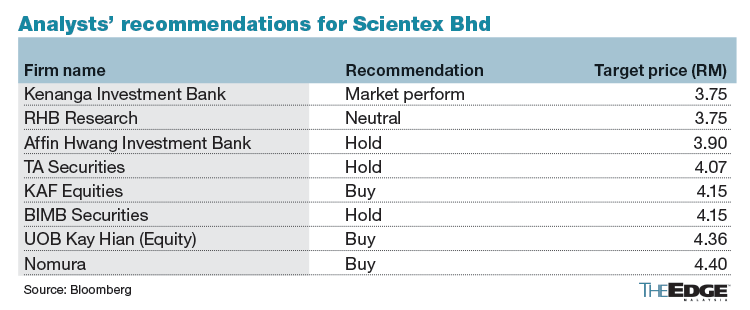

Kenanga Research maintained its ‘market perform’ rating for Scientex, and upgraded its target price (TP) to RM3.75, from RM3.63 previously, as the company expands its land bank.

Meanwhile, Kenanga Research also maintained its valuation basis of a price-earnings ratio (PER) of 12 times in FY2024 for Scientex's packaging business, at a premium to the sector’s average forward PER of 10 times to reflect its size, being one of the largest players in the region.

However, the research house cautioned that Scientex’s plastic packaging business, which contributes about a third of its earnings, is likely to be weighed down by the sluggish global economy over the near term.

Kenanga Research said risks for its call are a sudden spike in resin prices, weak consumer demand for packaging materials due to a prolonged global economic downturn, and high inflation, elevated mortgage rates and a weak job market, hurting demand for its properties.

The research house likes Scientex for its competitiveness in the global plastic packaging industry, given its size and low-cost structure, and its strong foothold in the affordable housing segment in Johor.

Meanwhile, TA Securities upgraded Scientex to 'hold' from 'sell', and said this is due to the recent decline in its share price, which triggered further upside. The house maintained its TP at RM4.07.

Scientex Bhd is a strategic partner with EdgeProp START, featuring the Mori Residences 2 development. All Scientex Bhd homebuyers also get to enjoy rewards worth up to RM18,888.

Looking to buy a home? Sign up for EdgeProp START and get exclusive rewards and vouchers for ANY home purchase in Malaysia (primary or subsale)!

TOP PICKS BY EDGEPROP

Semenyih Lake Country Club

Semenyih, Selangor

Mayfair Residences @ Pavilion Embassy

Keramat, Kuala Lumpur

Oxford Residences @ Pavilion Embassy

Keramat, Kuala Lumpur

Oxford Residences @ Pavilion Embassy

Keramat, Kuala Lumpur

{kind=link}