- “The group is actively seeking new lands with preference for large lands for township development, leveraging its strong balance sheet and expertise in the field.”

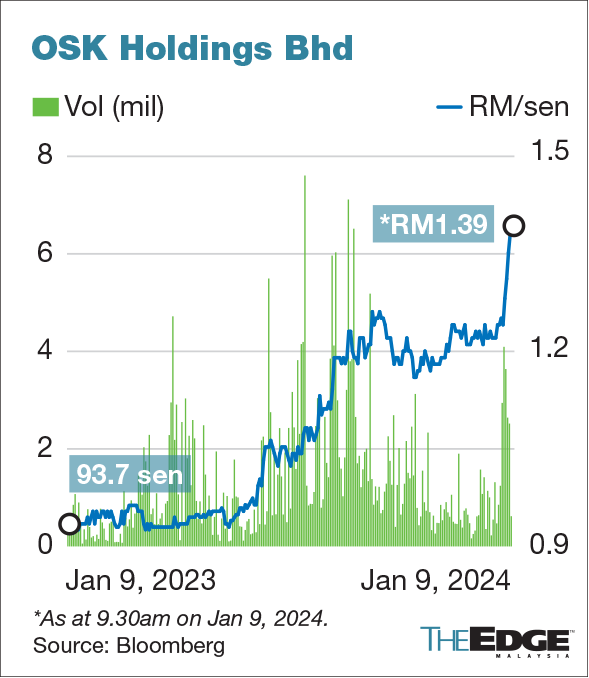

KUALA LUMPUR (Jan 9): Hong Leong Investment Bank Research (HLIB) has maintained its "buy" rating on OSK Holdings Bhd, with a higher target price of RM2.04 (from RM1.77) based on a 30% discount to a revised sum of part-derived valuation of RM2.91.

In a note on Tuesday, the research house said it anticipates a recovery in OSK’s property launches in 2024, as the group resolves some regulatory issues that have delayed several projects in 2023.

“The group is actively seeking new lands with preference for large lands for township development, leveraging its strong balance sheet and expertise in the field,” HLIB said.

For its cable segment, HLIB said the group currently enjoys industry-leading margins and is expanding its capacity and product range. Its new fibre optic line will also enable the group to tap into the lucrative telco segment, including tenders from Telekom Malaysia Bhd and other providers.

“OSK’s cable segment is undergoing expansion through (i) installation of a new fibre optic line, expected to be completed in early 2024, and (ii) addition of new machines, expected to arrive from 2Q2024 (second quarter of 2024) onwards and fully commissioned by end of 2024, adding 20%-25% to its current capacity,” HLIB added.

For its industrialised building system (IBS), HLIB noted that it is also undergoing capacity expansion through new machines and machine upgrades, which are expected to be completed in 2Q2024, boosting its capacity by 15%. The group’s IBS products are more environmentally friendly than conventional bricks, which gives them an edge in the green construction market.

“We believe the stock should gain increasing interest given that its own business segments, especially capital financing and industries, are demonstrating strong growth and should play a bigger role in contributing to the group’s earnings moving forward,” HLIB said.

According to the research house, OSK has a strong treasury team that capitalises on its extensive experience in the investment banking industry. With its robust balance sheet, the group has a lower cost of funding and a larger capacity for growth in its loan portfolio.

Looking to buy a home? Sign up for EdgeProp START and get exclusive rewards and vouchers for ANY home purchase in Malaysia (primary or subsale)!

TOP PICKS BY EDGEPROP

Persiaran Puncak Alam 6

Bandar Puncak Alam, Selangor

Bandar Botanic

Bandar Botanic/Bandar Bukit Tinggi, Selangor

hero.jpg?GPem8xdIFjEDnmfAHjnS.4wbzvW8BrWw)

{kind=link}