KUALA LUMPUR (Sept 10): Few may disagree that IGB Bhd signifies quality real estate assets given its track record, be it shopping malls or office space.

Hence, the lukewarm response to the units offered by its listing exercise of IGB Commercial Real Estate Investment Trust (REIT) is taken as a strong indicator of the hazy outlook on the domestic office space market, and investment money is shying away from the market segment, in which supply is expected to outstrip demand in the next three years, if not longer.

Adding to the pessimism is the expectation of the new norm — working from home — which would likely affect the demand pattern for office space.

Based on Knight Frank Malaysia's estimate, as at June 30, the cumulative supply of office space in Klang Valley stood at about 111.6 million square feet (sq ft) with the addition of 1.7 million sq ft of space from KL City.

By end-2022, an additional 10.13 million sq ft of office supply is scheduled for completion in Klang Valley.

"The under-subscription is reflective of the challenging office environment right now," said a property analyst who declined to be named.

Having seen the skyscrapers around the capital city Kuala Lumpur, such as 95-floor The Exchange 106 plus others in Tun Razak Exchange and PNB 118 (the tallest building in ASEAN), the analyst estimated that the office glut that started in 2014 will not ease in the next five to 10 years.

"After the pandemic, it will be a new norm for companies to downsize their office spaces, putting pressure on the office market which has already faced oversupply," the property analyst told The Edge.

While the supply keeps increasing, the demand is not growing as fast, partly because of foreign direct investment not driving much demand for office space, said the analyst.

The IGB Commercial REIT's assets include Menara IGB, IGB Annexe, Centrepoint South, Centrepoint North, Boulevard Properties, Gardens South Tower, Gardens North Tower and Southpoint Properties at MidValley City.

As at June, IGB Commercial REIT's average occupancy rate stood at 73.4%, down slightly from 76.3% in 2020.

The price of IGB Commercial REIT's institutional offering was fixed at 71 sen, lower than the indicative price of 83 sen set for its book-building exercise.

The restricted offer for sale (ROFS) for IGB Bhd's shareholders that came with distributions in specie was undersubscribed by 21.28%.

"Although IGB is a good sponsor, the office sector has been suffering from the supply glut for years, and the growth in terms of rental reversion has been lacklustre because of the oversupply issue," another analyst commented when contacted.

She shared the view that the culture of working from home amid the pandemic has negative impact on the office market.

"We don't know when the Covid-19 pandemic will end given the new variants, so the (continuation of) work-from-home trend would not be good for the office space demand in the near term," she added.

The analyst expected that some companies may opt to downsize office space for a combination of reasons including cost cutting and lesser number of staff working from office, on top of renegotiation for cheaper rental given the tenant market.

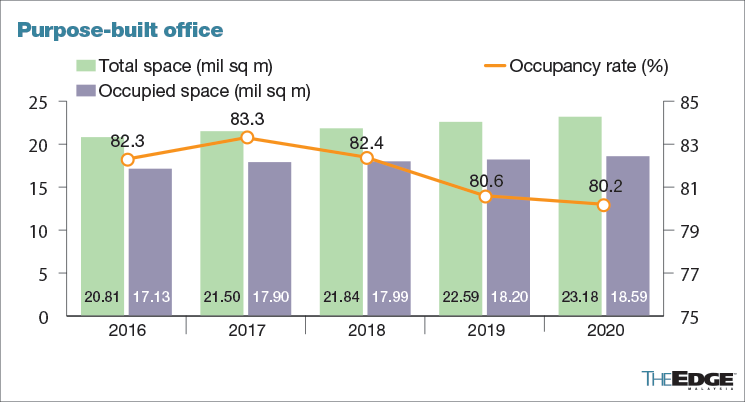

According to the National Property Information Centre, even before the Covid-19 pandemic, the occupancy rate of purpose-built offices had been on a declining trend, falling from 82.3% in 2016 to 80.2% in 2020.

The total office space available in the past five years has been on the rise. About 2.37 million square metres (sq m) had been added to the market from 2016 to 23.18 million sq m last year, versus 20.81 million sq m in 2016.

The occupancy rates for Kuala Lumpur and Selangor office spaces last year stood at 77.6% and 69.2% respectively, with total office space of 9.28 million sq m and 4.18 million sq m.

"The effects of the Covid-19 pandemic are seen on the overall market. There are lesser enquiries amid weaker office demand as the various strict containment measures (different phases of Movement Control Order) continue to impact the business operations of organisations.

"Many (prospective tenants) have decided to put on hold as they are not able to assess the office options holistically, for instance physical viewings were not allowed since June (until early this month)," said Knight Frank Malaysia's Corporate Services executive director Teh Young Khean.

However, he opined that the reopening of more economic sectors will hopefully help lift business sentiments.

"The lacklustre office market is expected to regain some momentum towards end 2021/early 2022 as the pent-up demand will drive companies to explore the market, especially those presently adopting a wait-and-see approach," Teh told The Edge.

According to him, the average rental and overall occupancy rate of office space in the Klang Valley continue to be under pressure due to the protracted Covid-19 impact.

Teh said, the office market in Kuala Lumpur remains challenging as supply continues to outstrip demand, placing significant pressure on rental and occupancy levels.

As of the second quarter of 2021, Kuala Lumpur had an average rental rate of RM6.84 per square foot with an average occupancy of about 68%.

The Kuala Lumpur fringe office market is, however, expected to remain steady despite the year being on a challenging mode due to its limited supply of good-grade office space.

The average rental is about RM5.67 per square foot, with an average occupancy of about 86%.

Well-maintained MSC buildings within transit-oriented developments such as KL Sentral, Mid Valley City, KL Eco City and Bangsar South will continue to be in demand, said Teh.

Fund managers contacted, however, are cautious about office REITs due to oversupply issues and the Covid-19 pandemic.

Fortress Capital Asset Management chief executive officer Thomas Yong said the sentiments towards the residential segment of the property sector have improved based on expectations of recovering demand and that affordability has been enhanced by the current easy monetary policies, however, the outlook for the office segment has remained poor.

According to him, this is a result of oversupply conditions, potentially further softening demand due to the developing work-from-home culture because of the Covid 19 pandemic.

He noted that IGB Commercial REIT would not be on his buy list any time soon.

Get the latest news @ www.EdgeProp.my

Subscribe to our Telegram channel for the latest stories and updates

TOP PICKS BY EDGEPROP

Seksyen 7, Kota Damansara

Kota Damansara, Selangor

Subang Perdana Goodyear Court 10

Subang Jaya, Selangor

Subang Perdana Goodyear Court 10

Subang Jaya, Selangor

Subang Perdana Goodyear Court 10

Subang Jaya, Selangor

Subang Perdana Goodyear Court 10

Subang Jaya, Selangor

Subang Perdana Goodyear Court 10

Subang Jaya, Selangor

Subang Perdana Goodyear Court 10

Subang Jaya, Selangor

{kind=link}