Malaysian Resources Corp Bhd (April 6, RM1.76)

Maintain buy with an unchanged target price (TP) of RM2.10: Malaysian Resources Corp Bhd’s (MRCB) recent joint venture (JV) with Adani Realty could spur its growth prospects by looking out for higher-margin projects and sharing its expertise in developing transit-oriented development (TOD) projects in India.

Projects developed by Adani Realty such as the upcoming Inspire BKC and Inspire Hub are both located in prime areas of Mumbai with access to public transport such as rail — drawing similar strength to MRCB albeit Adani’s lesser experience. Other property developers in India of similar stature such as Lodha Group and Oberoi Realty have similar project profiles in which MRCB could consider to impart its experience in TOD development.

We prefer MRCB to partner directly with Mumbai Suburban Railway to pass on its expertise. This would open up immediate access to developers with land or development close to the prime locations of Andheri, Bandhra and Mahalaxmi alongside the Western railway line in Mumbai.

Reliance Anil Dhirubhai Amabani Group (Reliance) has partnered with Samsung C&T India Pvt Ltd to build Dhirubhai Ambani International Convention and Exhibition Centre amounting to US$680 million (RM3.01 billion). The project is slated to be completed in the fourth quarter of 2017. Assuming the JV is on a 51%-49% basis on the back of a 9% profit margin, Samsung would stand to benefit US$29.9 million (49%) to its bottom line.

While we can only illustrate a comparable, it is expected that the JV for projects between MRCB and Adani would be formed on the same basis. We reckon that significant impact on earnings will only be meaningful to MRCB should the project clinched be more than US$600 million with profit margin assumptions estimated between 11% and 15.5%.

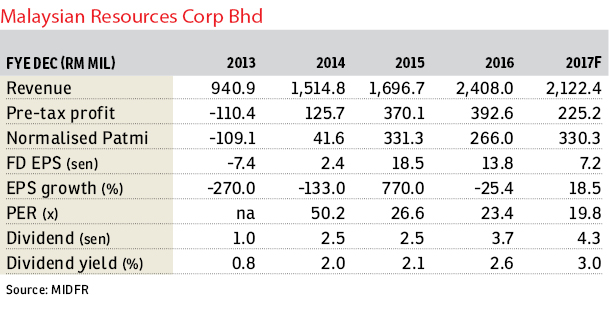

Given the prospect of TOD projects in Malaysia and India, MRCB shares are still attractive at 19.8 times forward earnings despite trading above its average three-year price-earnings ratio of 10.57 times. We maintain our “buy” call with an adjusted sum-of-parts based TP of RM2.10 per share, suggesting the shares have another 15.2% upside. — MIDF Research, April 6

This article first appeared in The Edge Financial Daily, on April 7, 2017.

For more stories, download TheEdgeProperty.com pullout here for free.

TOP PICKS BY EDGEPROP

Persiaran Damansara Indah

Tropicana, Selangor

Pangsapuri Andorra, Taman Sri Muda

Shah Alam, Selangor

Emira Residence @ Shah Alam

Shah Alam, Selangor

Bandar Bukit Raja

Bandar Bukit Raja, Selangor

Setia Taipan 1, Setia Alam

Shah Alam, Selangor

{kind=link}