KLCC Property Holdings Bhd (March 27, RM7.91)

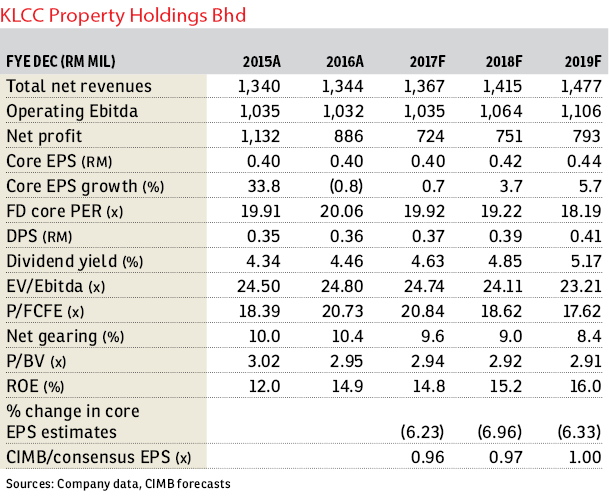

Maintain hold with a higher target price (TP) of RM7.69: Key takeaways from meeting KLCC Property Holdings Bhd (KLCCP) were: i) the office segment will see a mild dip in financial year 2017 forecast (FY2017F) due to a loss of income from Menara Exxon-Mobil; ii) the retail segment will be the main earnings driver in FY2017F, due to positive rental reversions and top-line growth from new tenants; iii) the hotel segment’s earnings in FY2017F will stay muted as Mandarin Oriental is undergoing guest room refurbishment; and iv) management service earnings will be boosted by additional facilities management services in Kerteh, Terengganu.

Occupancy of Menara Exxon-Mobil is currently 60% (versus 100% in FY2016), after the Exxon-Mobil lease expired in January 2017. We understand that management is identifying potential tenants for the vacant 40% and targets to maintain its long-term lease structure. As we assume occupancy will only rise gradually from the second half of FY2017F, we expect a 1% year-on-year (y-o-y) dip in the office segment’s core pre-tax profit in FY2017F from the loss of income, which would be slightly mitigated by additional net leasable area (NLA) of Dayabumi.

Suria KLCC’s average monthly rental rate of about RM30 per sq ft and tenant sales growth of 4% y-o-y in FY2016 reflect its super-prime location. We expect its occupancy rate to gradually rise to the historical average of 98% by end-FY2017F (versus 96% in FY2016), and forecast rental reversions of about 5% for one-third of NLA per annum as its tenancy profile improves. Its hotel segment is likely to stay muted with an average occupancy of 49% to 53% (FY2017F to FY2019F), until Mandarin Oriental’s room refurbishment is completed (in stages) by end-FY2018F.

We were too optimistic about our rental reversion assumptions for the retail segment and occupancy rates for the office segment, particularly for Menara Exxon-Mobil. As such, we cut our FY2017F to FY2019F earnings per share by 6% to 7%. Furthermore, we revised our dividend discount model (DDM) assumptions, reducing the discount rate to 7.4% from 7.8% as the equity risk premium narrowed — given the recent rerating of the FBM KLCI — and increased our terminal growth assumption to 2.1% (versus 1.7% previously).

We maintain “hold” with a higher DDM-based TP of RM7.69. We believe KLCCP’s share price has always traded at a premium over its peers due to its size, prime location and secured office assets that are locked in triple net leases, as well as the strong brand name of its retail assets. As such, its earnings are more resilient and sheltered from a downturn in the office and retail segments, compared with its peers. An upside risk is an earlier injection of potential assets. A downside risk is lower-than-expected occupancy rates. — CIMB Research, March 26

This article first appeared in The Edge Financial Daily, on March 28, 2017.

For more stories, download TheEdgeProperty.com pullout here for free.

TOP PICKS BY EDGEPROP

De Cendana Apartment

Setia Alam/Alam Nusantara, Selangor

Bandar Baru Sri Petaling

Bandar Baru Sri Petaling, Kuala Lumpur

{kind=link}