Eco World Development Group Bhd (Jan 23, RM1.35)

Maintain buy with an unchanged target price of RM1.80: A relatively new property developer with only three years of history, Eco World Development (EcoWorld) has been able to sell properties at an unprecedented pace, reflecting property buyers’ confidence in the group’s strong brand name.

After booking RM3.2 billion/RM3 billion/RM3.8 billion gross sales in financial year 2014 (FY2014), FY2015 and FY2016 respectively, EcoWorld is targeting RM4 billion gross sales in FY2017 (including joint-venture portion) despite the relatively weak property market where most of its peers are having slower sales performance. EcoWorld has clearly been gaining more market share at the expense of its competitors.

This will be anchored by 15 ongoing projects and two new projects to be launched in FY2017 (Eco Forest@Semenyih, Selangor and Eco Horizon@Batu Kawan, Penang). Riding on its strong brand name, EcoWorld continues to rely entirely on its internal marketing and sales team though we have seen some developers increasingly engaging external property agents to market their products.

We believe its innovative township products will remain well-received in the market as its townships continue to gain traction with more deliveries completed. There would be more than 4,700 units to be completed in FY2017 which could help get more interest from potential buyers.

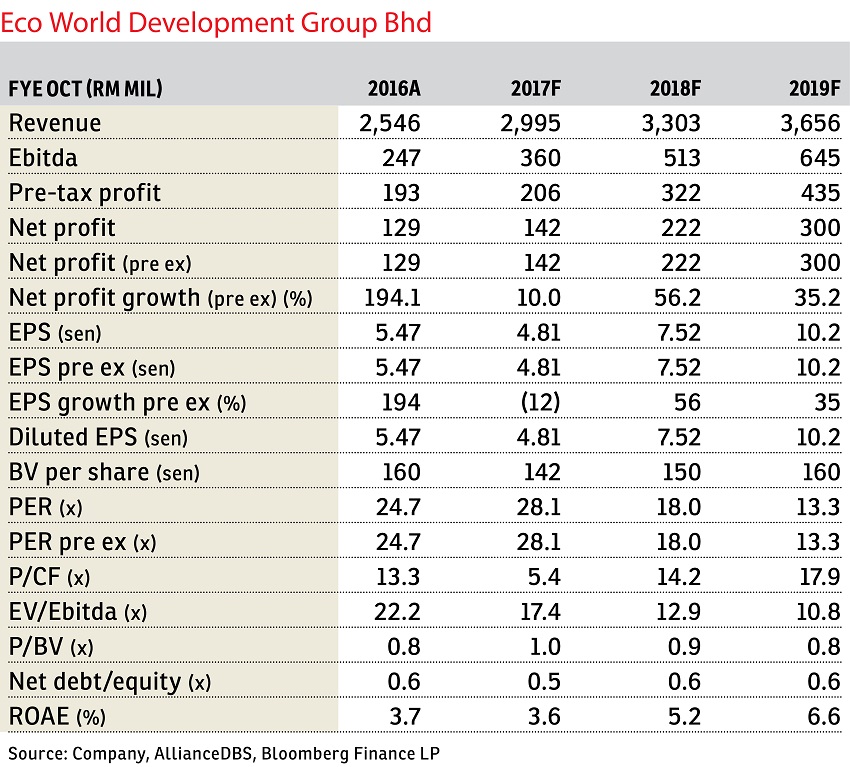

We are projecting an explosive three-year earnings compound annual growth rate (CAGR) of 33% over FY2016 to FY2019, due to its relatively smaller profit base at this juncture. This is supported by its all-time high unbilled sales of RM4.9 billion as at end-Oct 16 which will underpin earnings up to FY2019.

In anticipation of better cash flow with the handover of completed units as well as the completion of a proposed private placement by the first quarter of calendar year 2017, EcoWorld’s balance sheet is expected to remain healthy and accommodative for its aggressive expansion plans.

EcoWorld is looking to venture overseas via a proposed subscription of a 27% stake in Eco World International Bhd (EWI) by March 17, which has significant exposure to London and Sydney with total property sales of RM5.3 billion as at Oct 16. This will further cement its earnings growth from FY2018 onwards upon completion of projects, though EWI will incur losses in FY2017.

Sales performance at EWI in London had not been affected much in 2016 despite Brexit. In fact, the 2016 UK property sales of £441 million (RM2.45 billion) were higher than its 2015 sales of £436 million.

We believe EcoWorld deserves to trade at a lower discount relative to its peers given its prominence as the bellwether of the Malaysian property sector with ongoing outperformance in a weak market. We continue to like EcoWorld for the proven and impeccable track record of its key senior executives, who have helped the developer to establish strong brand recognition among property buyers.

2018 will start to see lower gearing when more township projects enter more matured phases which will be cash-generative. Earnings will be driven by 17 ongoing Malaysian projects as well as EWI’s maiden profit contribution after the start of the handover of London projects. We are projecting three-year earnings CAGR of 32% which exclude EWI’s contribution for now, pending the release of its initial public offering prospectus. — AllianceDBS Research, Jan 23

This article first appeared in The Edge Financial Daily, on Jan 24, 2017. Subscribe to The Edge Financial Daily here.

TOP PICKS BY EDGEPROP

Duduk Huni @ Eco Ardence

Setia Alam/Alam Nusantara, Selangor

Irama Perdana @ Alam Perdana

Bandar Puncak Alam, Selangor

Saville @ The Park

Pantai Dalam/Kerinchi, Kuala Lumpur

Pangsapuri Enggang

Bandar Kinrara Puchong, Selangor

De Cendana Apartment

Setia Alam/Alam Nusantara, Selangor

Pangsapuri Seroja

Setia Alam/Alam Nusantara, Selangor

{kind=link}